Did Infrastructure-Funded Demand Visibility Just Recast Vulcan Materials’ (VMC) Long-Term Investment Narrative?

Long-Term Investment Narrative?")

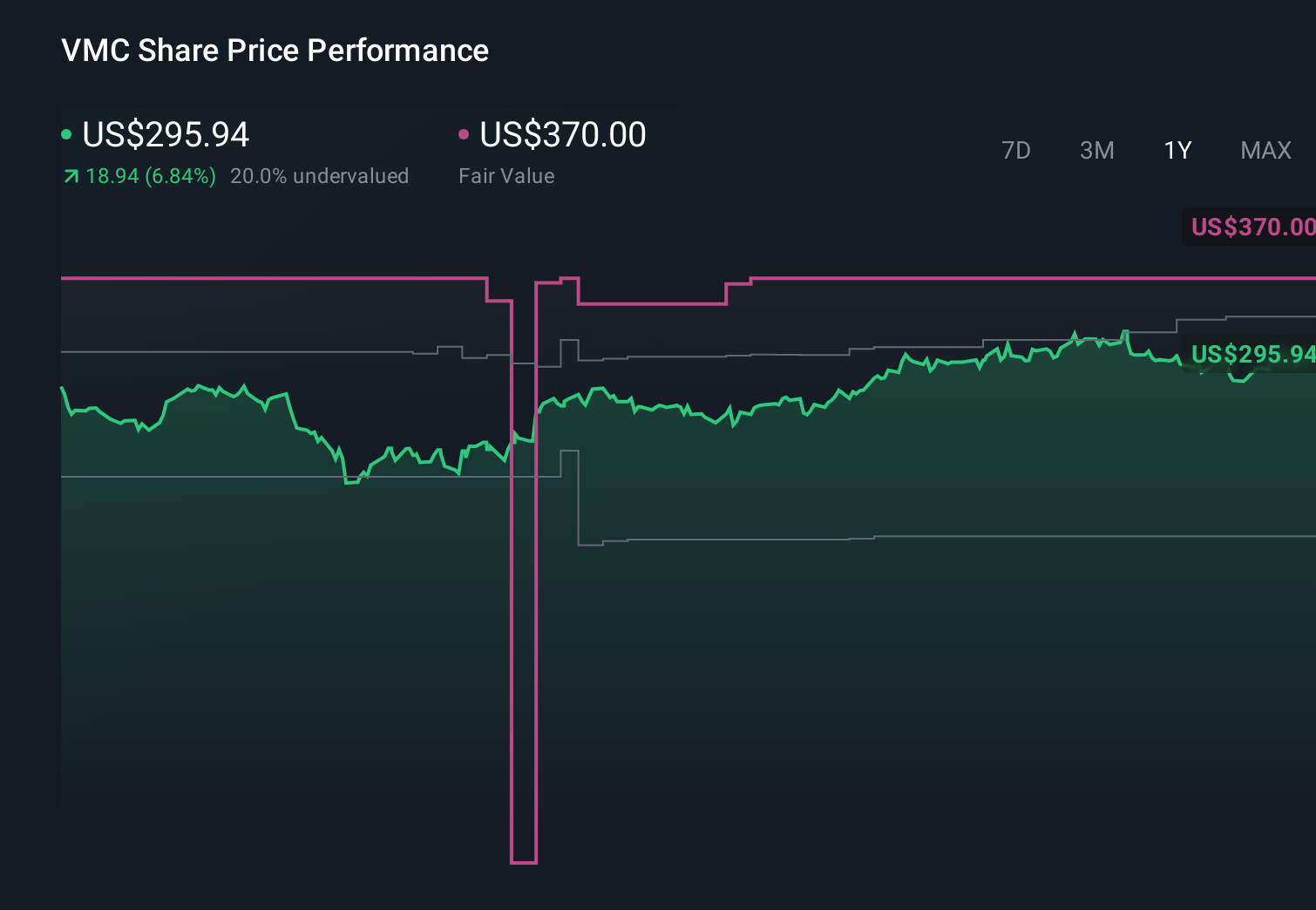

- Recent commentary on Vulcan Materials highlighted how the company is benefiting from resilient construction and infrastructure demand underpinned by multi-year federal and state funding programs, alongside disciplined pricing and operations.

- An interesting takeaway is that analysts see Vulcan’s exposure to publicly funded infrastructure and high-growth regions as giving it unusually clear visibility on aggregates demand.

- We’ll now look at how this infrastructure-driven demand visibility shapes Vulcan Materials’ investment narrative and longer-term positioning.

AI is about to change healthcare. These 108 stocks are working on everything from early diagnostics to drug discovery. The best part – they are all under $10b in market cap – there’s still time to get in early.

What Is Vulcan Materials’ Investment Narrative?

To be comfortable owning Vulcan Materials, you need to believe that federally and state-funded infrastructure, plus reasonably healthy construction activity, can keep underpinning steady aggregates demand even if the broader economy slows. The latest commentary reinforces that story, pointing to multi-year public funding and disciplined pricing as support for volumes and margins, which aligns with Vulcan’s recent earnings momentum and the stock’s climb. In the near term, the key catalyst is whether upcoming results on February 17 confirm that pricing power and infrastructure-backed shipments are holding up. The news also slightly reframes risk: with the share price already trading on a premium multiple and near analyst targets, any disappointment on volumes, bidding activity, or cost control could matter more than before.

However, there is a less obvious risk around Vulcan’s high valuation that investors should not ignore.

Vulcan Materials’ shares are on the way up, but they could be overextended by 15%. Uncover the fair value now.

Exploring Other Perspectives

Four Simply Wall St Community fair value estimates span roughly US$115 to US$321.5, underlining how far apart individual views can be. Set against a premium valuation and heavy reliance on infrastructure funding, this dispersion invites you to weigh how much optimism is already in the price.

Explore 4 other fair value estimates on Vulcan Materials – why the stock might be worth less than half the current price!

Build Your Own Vulcan Materials Narrative

Disagree with this assessment? Create your own narrative in under 3 minutes – extraordinary investment returns rarely come from following the herd.

Ready To Venture Into Other Investment Styles?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We’ve created the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Try a Demo Portfolio for Free

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email [email protected]

link

:max_bytes(150000):strip_icc()/Roi-5c4a640a34204da285b4ef1c98970be0.png "What Is Return on Investment (ROI) and How to Calculate It")